Strategy Update / Click here for full PDF version

Author(s): Jovent Muliadi ; Axel Azriel

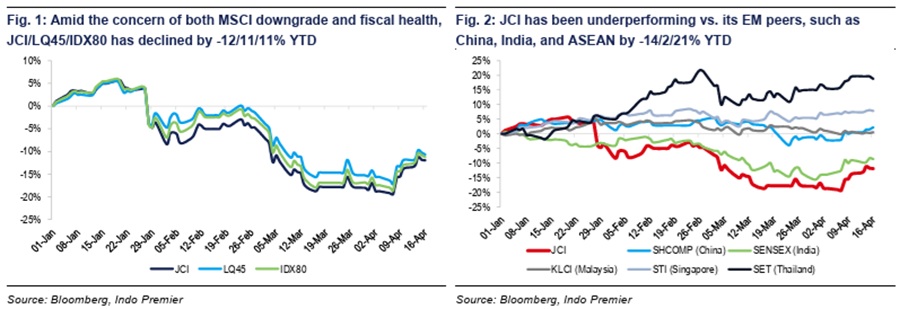

- JCI/LQ45 has dropped by -12/-11% YTD, underperformed its EM peers like China/India/ASEAN peers by -14/-2/-21% YTD.

- This was attributed to concerns on: 1) MSCI downgrade to Frontier market and 2) widening fiscal deficit amid on-going Middle East tension.

- We think with the weakness on yield/Rupiah, commitment to maintain the deficit <3%, and potential beat in 1Q results shall result in JCI reversal.

YTD was a perfect storm for JCI

JCI/IDX80/LQ45 dropped by -12/-11/-11% YTD due to combination of: 1) concern on MSCI downgrade to frontier market (link to our report) back in Feb and 2) concern on fiscal health which also led to outlook downgrade by rating agencies (Fitch and Moody's.); this was also exacerbated by concern on widening cost for fuel subsidy amid ongoing Middle East tension. This has resulted in underperformance vs. China/India/ASEAN peers by -14/-2/-21%.

We expect most of the concerns will at least somewhat be resolved in the near term

Our conversations with foreign investors suggested that the risk of downgrade to Frontier market is very minimal especially post MSCI warning that has resulted in JCI attempt to have better disclosure i.e. increasing the shareholders categories to 39 from 9 and disclosure for >1% ownership; along with creation of high shareholding concentration list (similar to HK). Most investors think that this is already good enough vs. its EM peers. Separately, MoF also committed to maintain overall deficit to be below 3% - even under scenario that oil price averaged at US$100/barrel vs. current average at c.US$80/barrel. Based on our channel check this will be achieved through 1) optimization in free meal program, 2) budget cuts across ministries and 3) smaller tax restitution.

Further rating downgrade is consequential; government commitment to maintain fiscal deficit <3% is imperative

Bond yield has derated to 6.9% from 6.1% at end-Dec25, before rebounded to 6.6% whereas Rupiah has weakened by -3% YTD (vs. INR/THB which depreciated by -4%/-2% YTD while RMB/MYR has strengthened by +2%/3% YTD), which clearly showed that market has slowly started to priced-in the fiscal risk. Our analysis suggests that rating downgrade to junk for other countries resulted in 260/820/640bp gradual increase in bond yield in Morocco (spike in inflation)/Colombia (expansionary fiscal policy)/Russia (sanctions from Ukraine war) in Apr21/Jul21/Mar22. As such, Government commitment to maintain fiscal deficit at <3% of GDP is imperative to maintain the investment grade.

Earnings growth clearly is underappreciated; 1Q may surprise which shall be the catalyst for reversal

We expect companies under our coverage/LQ45 to deliver +10/16% earnings growth this year after booking -2% growth in FY25. This is higher than consensus expectation for China/India/Malaysia/Thailand of 9/9/7/7% and we also expect a beat against consensus expectation in 1Q26 results for banks, commodities i.e. metals/coal and consumer. Our picks are , , , for banks; , , (NR) for metals, for coal; and for consumer.

Sumber : IPS